The Value-Based Purchasing Math Problem

Successful Value-Based Purchasing initiatives carefully allocate dollars across Funding Pools to achieve the proper balance of spending on prevention, early intervention, health home services, acute care, etc. This is described in more detail in the System Modeling Section of this Toolkit.

Each Funding Pool should be built around a Utilization and Cost Budget that is then translated into one or more Accountable Payment Models for the services in the Funding Pool. Note that all Accountable Payment Models come from the same math problem.

Let’s use an Outpatient Behavioral Health service area to illustrate how this works.

Each Funding Pool should be built around a Utilization and Cost Budget that is then translated into one or more Accountable Payment Models for the services in the Funding Pool. Note that all Accountable Payment Models come from the same math problem.

Let’s use an Outpatient Behavioral Health service area to illustrate how this works.

Step 1: Identify the Population: ABC RBHA serves 10,000 Medicaid enrollees and is responsible for providing all health and behavioral healthcare to these individuals.

Step 2: Estimate the Behavioral Health Penetration Rate: ABC RBHA uses historical data to estimate how many of the enrollees will need behavioral health services in the upcoming budget year. Since one can never predict the future with great precision, three scenarios are developed.

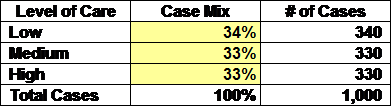

Step 3: Estimate the Case Mix: What is the acuity mix and how will those using care distribute across the levels of Care? The following example is for the Medium Penetration Rate Scenario.

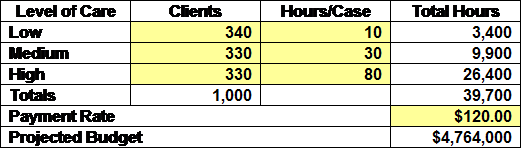

Step 4: Estimate Utilization: What is the average utilization at each level of care?

Step 5: Estimate the Unit Cost/Fee: What is the average cost per hour across all disciplines that should be factored into the model?

Step 6: Compute the Anticipated Costs: What is the anticipated Outpatient Behavioral Health Costs for a Scenario that is based on the Medium Penetration Rate, Average Hours, and the Medium Payment Rate?

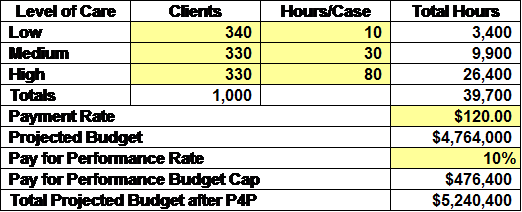

Step 7: Determine the Pay for Performance Budget: What will be placed in a P4P Budget that will be allocated to providers if the identified performance measures are met or exceeded?

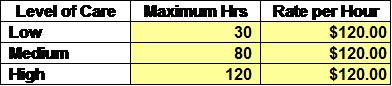

Step 8: Determine the Payment Rates: Utilizing the assumptions in Steps 1-6, what are the Payment Rates under each Accountable Payment Model?

Modified Fee for Service: The following rate will be paid as long as the hours per case do not exceed the maximum hours at each Level of Care:

Modified Fee for Service: The following rate will be paid as long as the hours per case do not exceed the maximum hours at each Level of Care:

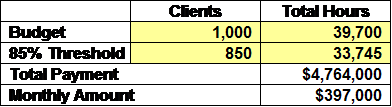

Capacity Funded: The following rate will be paid as long as the number of cases served exceed 85% of the anticipated cases and the hours of service exceed 85% of the anticipated hours.

Case Rate/Bundled Payment: The following rates will be paid as long as the average hours per case at each Level of Care exceed 85% of the average hours for that Level.

Sub-Capitation: The following rate will be paid as long as number of cases served exceed 85% of the anticipated cases and the hours of service exceed 85% of the anticipated hours.

Lessons Learned: The critical lessons from this exercise are twofold:

- It is necessary to project utilization and cost for each service area, regardless of the payment model being considered.

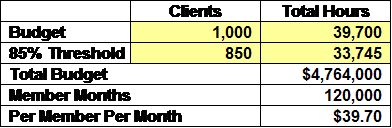

- The same amount of money is anticipated to be spent ($4,764,000) under each of the Accountable Payment Models, before the Pay for Performance payments are distributed.